Concerns with Tender Requirements

An ongoing issue of concern to the tax stamp world has recently resurfaced.

The issue refers to the recent release of tax stamp tender specifications for Oman, which appear to eliminate all but a seemingly preselected supplier, thereby rendering what should be a competitive tender almost non-competitive.

The tender – which is entitled ‘Digital Tax Stamp Solution for Excise Goods’ – will allow Oman to introduce tax stamps for the first time.

One concerned solution provider told Tax Stamp & Traceability News™ (TSTN) that the supplier preconditions laid out in the tender favour only one, or possibly two, of the larger suppliers, and knock out all the rest.

For instance, the tender obliges bidders to possess minimum qualifications that include:

Participation as a manufacturer and prime contractor in at least three existing digital tax stamp contracts, with a total contracted volume in excess of 1.5 billion stamps per annum.

Minimum of three existing security product contracts within the region where the country issuing the tender is located. These contracts can include tax stamps, postage stamps, passports, government security documents or banknotes.

In addition, the time given for suppliers to prepare their bids was only three weeks, which was considered too short for many suppliers (for most tax stamp tenders, the time allotted ranges from 3-6 months).

Opposing forces

Tax stamp programmes are often heavily opposed by those industries that must comply with the legal and technical requirements of the programmes. It is common for these industries to exert their considerable economic and political clout to avoid regulation, and there are many well documented instances of significant lobbying efforts and other industry tactics being brought to bear on tax stamp and traceability programmes.

Tax stamp solution providers, as an industry in their own right, should therefore not provide any fodder to the already considerable opposing forces that normally exist in this market.

Ensuring a level playing field

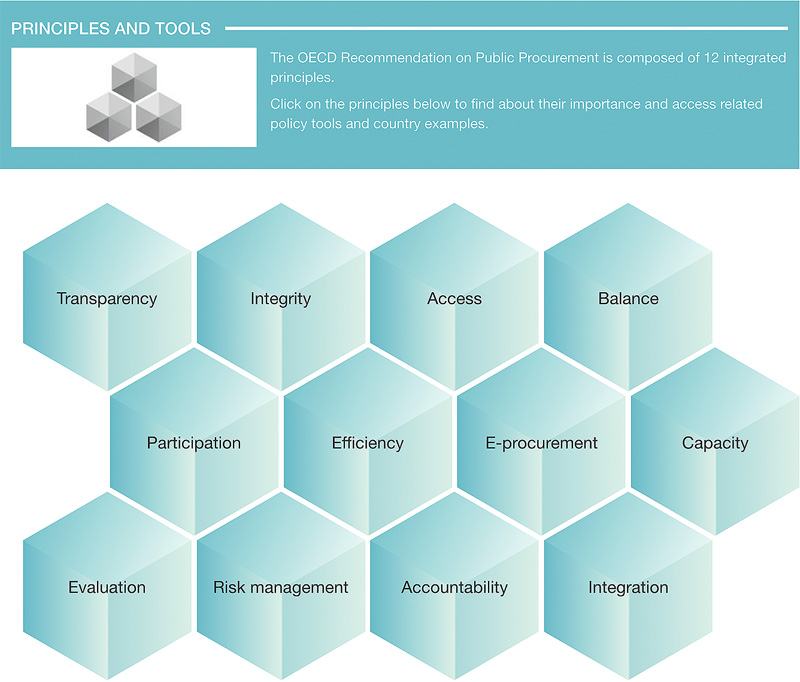

In his article ‘Writing an RFP for Tax Stamps and Traceability Systems,’ (TSTN, September 2020), Ian Lancaster, Associate, Reconnaissance International, referred to a ‘toolbox’ of 12 integrated principles – compiled by the Organisation for Economic Co-operation and Development (OECD) – which are key to establishing a fair and transparent tender process.

The principles in question are: transparency, integrity, access, balance, participation, efficiency, e-procurement, capacity, evaluation, risk management, accountability and integration.

For the purpose of this article, the principle which concerns us is ‘access,’ which refers to the creation of a level playing field for potential suppliers to gain access to government contracts.

Such access remains a major hurdle, stated Ian, with SMEs (small and medium-sized enterprises) often representing a very low share of government contracts. These smaller companies can often meet with obstacles relating to regulatory burden, financial constraints, lack of technical expertise, and the obligation to pay to participate in public procurement processes. The problem is therefore a widespread one that is by no means specific to tax stamp systems.

In order to address this issue, the OECD urges governments to:

Have in place coherent and stable institutional, legal and regulatory frameworks, which are essential to increasing participation in doing business with the public sector.

Deliver clear and integrated tender documentation, standardised where possible and proportionate to the need.

Use competitive tendering and limit the use of exception and single-source procurements. (Competitive procurement involves opening the process to bids and tenders to obtain the best value, while non-competitive procurement happens when the buyer either selects the company to buy from or restricts the bidding process to certain suppliers).

Complying with these recommendations would go a long way to avoiding the type of situation described in this article, as well as the situation in Nepal and Pakistan.

The OECD Toolbox website can be found at www.oecd.org/governance/procurement/toolbox/principlestools/. Clicking on one of the cubes opens detailed explanation and guidance.

Subscriber content

Read the full article

Full access to Tax Stamp & Authentication News™ articles, newsletters and archives.