Economists in Chile Report Higher Cigarette Revenues and Lower Returning Exports

As a large number of Tax Stamp & Traceability News™ readers are already aware, tobacco and alcohol producers spend significant amounts of time and effort lobbying against the installation of tax stamp and traceability systems that are fully managed by national revenue authorities.

The producers’ recurrent argument against such systems is that they are expensive and, more importantly, don’t offer better performance with respect to controlling tax revenues than systems owned and operated by the producers themselves.

A recent study by economists Guillermo Paraje, Luca Pruzzo and Mauricio Muñoz, all from the Business School at Universidad Adolfo Ibáñez in Chile, says otherwise. Published in April of this year, in www.tabaconomia.uai.cl, the study draws some positive conclusions for those of us who agree that independent, high-security tax stamp and traceability systems provide the best mechanism for improving tax revenues and helping countries to reduce illicit trade.

Universidad Adolfo Ibáñez is a private Chilean university that was recently selected to work in Latin America as a partner of Bloomberg Philanthropies’ initiative to reduce tobacco consumption on a worldwide basis. It is noteworthy that as of the publishing date of the study, the Chilean government had not publicly released its evaluation of the impact of its traceability system (called SITRAF – Sistema de Trazabilidad Fiscal) with respect to either increased revenues or illicit cigarette activity.

Following a lengthy tender process, Chile implemented SITRAF in May 2019, in compliance with the Framework Convention on Tobacco Control (FCTC), which it ratified in 2005. The goal of the programme was to help control the complete distribution and sales chain for tobacco products in Chile.

Tax on cigarettes in Chile is applied as a specific tax per cigarette as well as an ad valorem component. These taxes combined represent approximately 75% of the cigarette retail sales price.

Under SITRAF, each cigarette pack produced on domestic manufacturing lines is marked, directly at the factory, with a unique code printed with security ink, prior to being distributed. As for imports, they are marked at origin by foreign manufacturers, with a stamp that includes the same unique secure code and material security features. The quantity of packs marked is then transmitted in real time to the Chilean tax authority (SII – Servicio de Impuestos Internos).

Before SITRAF, the quantity of cigarettes and brands produced and commercialised were advised directly by the producer to SII, allowing little opportunity for the tax authority to verify the accuracy of the numbers reported and to reconcile them with taxes paid.

Recent tax revenues and cigarette quantities

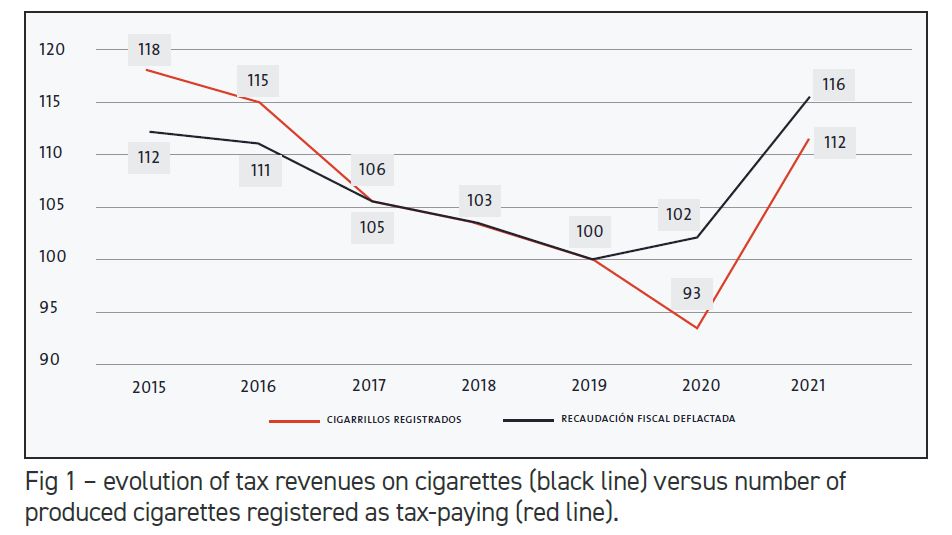

Using 2019 = 100 as the base, Fig 1 of the study shows the evolution of tax revenues on cigarettes (black line) versus the number of cigarettes produced that were registered as tax-paying (red line). It is notable that, in 2020 and 2021, real tax collection increased despite a lower amount of cigarettes sold.

The increase in revenue in 2020 is significant, as despite an important reduction in the consumption (production) of cigarettes that paid taxes, it implies that there was a sharp increase in cigarette prices, something which could explain the increase in revenue, as the ad valorem component of the cigarette tax depends on quantity and price.

Another insight from Fig 1 is the marked growth in the number of cigarettes that effectively paid taxes in 2021, the first increase for this number since 2012. The study postulates two potential, non-exclusive, reasons for this increase: growth in tobacco usage and/or a reduction in illicit cigarette sales, possibly as a result of better enforcement of taxes paid.

However, given that tobacco usage in Chile remained relatively constant during 2020-2022, the finger points to decreased illicit trade as the reason for the growth in taxes paid.

Another clue is that Chile’s tobacco exports, which are exempt from all in-country taxes levied on tobacco, have become visibly differentiated from those produced for internal consumption (which are now marked), making illegal re-entry of cigarettes destined for external sale more complex – something that was quite easy to do prior to SITRAF.

Furthermore, cigarette exports from Chile fell by 10% between 2019 and 2020, and by 38% between 2020 and 2021, when the traceability system was already in full force.

Evolution of real prices for legal cigarettes

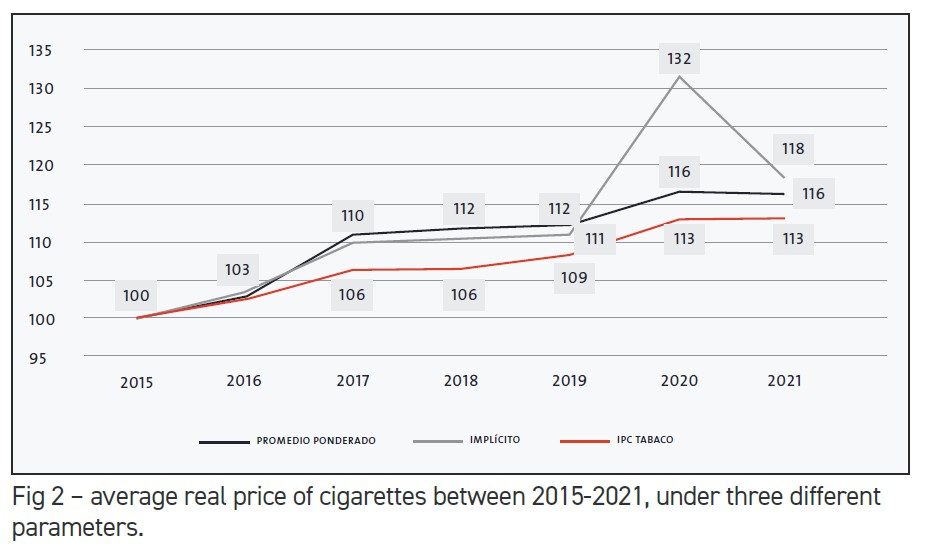

A more complex scenario can be seen in Fig 2, which shows the average real price of cigarettes between 2015-2021, under three different parameters.

The red line shows the official government calculation of cigarette prices, based on the tobacco component of the consumer price index (IPC) as calculated by the National Statistics Institute of Chile (INE). This line indicates a constant increase in the real price of cigarettes which, in 2021, was 13% higher than that recorded in 2015.

The black line is the average real price of cigarettes estimated using the official sales prices published by SII throughout 2015-21, weighted according to brand sales reported by Euromonitor International, and adjusted for inflation using the IPC.

Finally, the grey line shows the evolution of the implicit real price of cigarettes obtained by taking into account the collection of the ad valorem component of the cigarette tax. We can clearly see that 2020 shows a significant increase, well above that recorded in other years.

In 2021, there is an inexplicable drop, which is odd given that nominal prices did not decline between 2020 and 2021 and the inflation rate was not high enough to explain this drop.

One theory could be that cigarettes of relatively cheap brands in the domestic market, which until 2020 were perhaps destined only for export, have been re-directed to the domestic market, lowering this price and probably displacing some of the more high-end brands that were previously sold illicitly in-country.

Evolution of real tax revenues

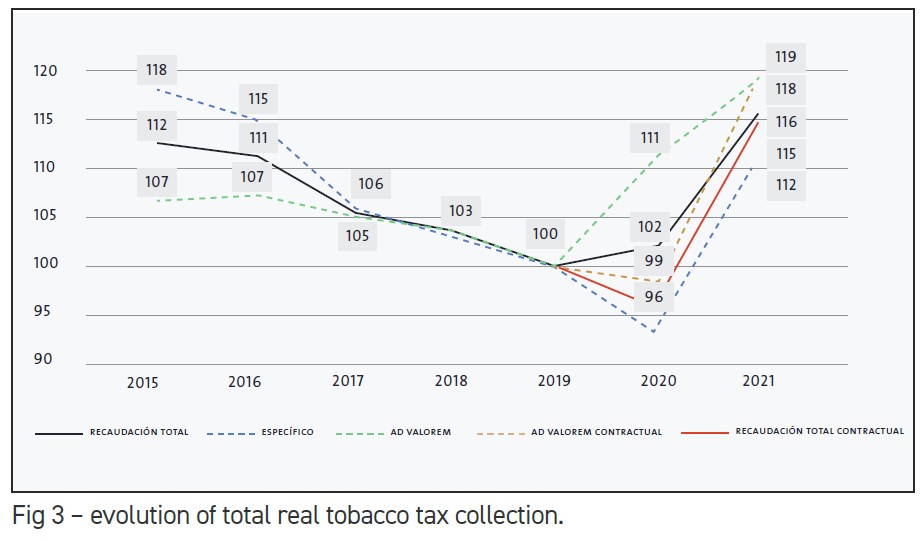

The final analysis by the economists, depicted in Fig 3, shows the evolution of total real tobacco tax collection (black line) and its specific and ad valorem components (blue and green dotted lines, respectively), between 2015-2021.

Fig 3 shows that between 2015-2019, total real collection decreased consistently, and that the specific component of tobacco tax collection was above, or equal to, that of the ad valorem component. However, beginning in 2020, the first full year of operation of SITRAF, total real tax collection increased, and the ad valorem component significantly exceeded the specific component.

As surmised earlier in this article, the increase in real prices implicit in the collection of the ad valorem component in Fig 3 for 2020 reflects, precisely, the accurate estimation of what is produced for domestic sales (and not the companies’ self-reporting).

There are two additional lines in Fig 3 that are also key to understanding the cost-efficiency of a traceability system. The dashed orange line shows what the real tax collection of the ad valorem component would have been if the real collection of this component had behaved as it did until 2019, relative to the specific component. The solid red line shows the evolution of total real revenue by adding the specific component and the counterfactual of the ad valorem component.

Now, comparing the green dotted line with the orange dotted line gives an estimate of the increase in revenue obtained by the ad valorem component from the full operation of the new traceability system. Likewise, comparing the solid black line with the solid red line estimates the increase in revenue, but for the total real tax collection.

Finally, taking into consideration the differences between the latter two series and the total real tax collection obtained in 2021, it would be possible to estimate that, purely as a result of the change in the evolution of the ad valorem component of the tobacco tax, the SII would have collected an additional 75.7 billion pesos (constant 2022), equivalent to $85.9 million, or 3.2% of the total collection in 2020 and 2021.

Conclusions

The points that drive home the study’s positive evaluation of Chile’s traceability system are:

Real tax revenue from tobacco taxes increased by 16 percentage points between 2019 and 2021, which is attributed, at least initially, to a strong increase in the average real price implicit in the payment of the ad valorem component of this tax.

In simpler terms, the SITRAF system’s accurate reporting of data has made certain that the tobacco industry reports its real total production, and therefore, pays the respective tax. Higher collection of the ad valorem component indicates accurate control over the mix of brands/prices effectively produced and sold domestically.

The increase in the quantity of cigarettes produced for the domestic market during 2021, which grew for the first time since 2014, is also striking. If this increase is due to better control by SII of the tobacco industry’s numbers, then it points to the possibility that prior to the implementation of the new traceability system, the tobacco industry did not adequately report the value of its production destined for the domestic market or for export.

The drop in exports could also be due to the current unique marking of cigarettes for the domestic market, which makes their illicit re-entry more difficult. It’s not irrational to surmise that prior to SITRAF, demand for well-known brands could be satisfied with cigarettes produced domestically, under-declared to the tax authorities, exported, and re-entered illicitly for sale, so as to avoid the tax. As mentioned earlier, with SITRAF, the number of cigarettes produced is informed to the tax authority in real-time at the moment of production.

The study concludes that the SITRAF system has indeed increased fiscal control over the tobacco industry in Chile, and although there are no official announcements from SII on this matter, one would hope that these results should help to promote the implementation of a similar traceability system for alcoholic beverages. All that’s missing for that to happen is for SII to say the word.

Subscriber content

Read the full article

Full access to Tax Stamp & Authentication News™ articles, newsletters and archives.