Tax and Customs Administration: Trends Shaping 2023

Across tax and customs administrations, there are several key trends that are of some relevance to the secure marking and traceability space.

Some of these are, to a greater or lesser extent, perhaps already referenced in secure marking and traceability solutions. However, a large part of the art of the pitch lies in speaking language that tax and customs administrations understand, and in using terms and constructs they are already familiar with. It lies in showing how solutions are about more than simply securing a revenue stream but instead are about empowering administrations to fulfil their obligations more holistically.

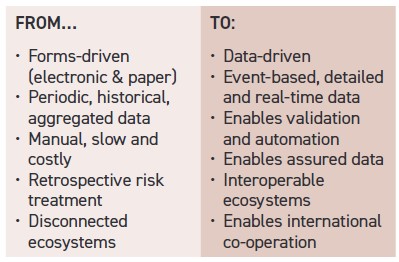

Tax Administration 3.0

Tax Administration 1.0 – the traditional approach to tax administration – relied on manual processes, lacked the use of technology or data analytics, and was characterised by a lack of transparency and accountability.

Modern tax administration is moving towards the OECD’s newer standard – Tax Administration 3.0 – which seeks to transform the way governments collect and manage taxes. It focuses on technology, data analytics, artificial intelligence, transparency, and accountability.

Tax 3.0 requires the introduction of greater verified reporting through third parties, as well as the adoption of more reliable reporting systems (eg. the digitalisation of VAT invoices, online cash registers, the building of basic tax rules into accounting software), and the improved detection of non-compliance through better risk modelling. The aim is to transform the payment of taxes into a seamless experience that is integrated into daily business activities.

Done correctly, secure marking and traceability initiatives can help administrations on their journey to meeting 3.0 standards.

A new draft tax convention

Until now, the OECD has played a leading role in driving the standardisation of tax policy development, but there is growing scepticism about the impact the organisation has practically had on curbing tax abuse. As a result, the space is rapidly changing, with the UN resolving at the end of 2022 to take over the tax leadership role from the OECD.

As part of the UN’s strategic positioning, it has published its own draft tax convention. This constitutes a rare opportunity to engage on good practices that should be adopted by tax administrations globally and to fundamentally change the way administrations understand the tools and options at their disposal with regard to – for instance – safeguarding supply chains in order to curb tax abuse.

Compliance by design

Historically, tax and customs administrations tended to view enforcement as their primary compliance tool – in other words, getting taxpayers and traders to do the right thing by purely relying on audits and investigations.

More recently, administrations have been developing strategies that build compliance into systems from the start. ‘Compliance by design’ is about setting up systems and processes to minimise human intervention; introducing governance and controls into every step of every process; making it easy for taxpayers and traders to do the right thing; and making it easy to spot anomalous, higher risk behaviours automatically.

For providers of traceability solutions, this requires a sensitivity to the impact that each step in a producer’s or importer’s lifecycle and value chain has on the likelihood of them being compliant – and on the ability to match and mine data in near-real time.

Two related concepts are featuring increasingly strongly in administrations’ repertoires:

Cooperative compliance programmes, which seek to foster a more transparent relationship between tax administrations and taxpayers, using proactive approaches to resolving material tax risks, before tax returns are even completed.

Authorised economic operator programmes, which acknowledge sound risk management practices by traders by reducing the regulatory burden on them.

All these programmes rely on an administration’s ability to distinguish between high-risk taxpayers and traders, and lower risk ones, and then developing differentiated treatment options for the different risk categories.

For a secure marking and traceability programme to truly add value, it needs to support administrations in assessing the risk profiles of taxpayers and traders, with reference to historical compliance data; the ability to establish industry norms and patterns against which outliers and anomalies can be detected; and with the ability to match and mine big data sets beyond simply excise data.

Digitisation

Digitisation is an obvious avenue for tax and customs administrations because it reduces turnaround times, reduces error rates, reduces opportunities for integrity issues, and (over time) reduces administrative costs.

Despite this, many administrations still grapple with manual processes and legacy systems. This is particularly true for excise administrations, which are often one of the last functions to be modernised, as they are not necessarily always big revenue contributors. (Tax administrations may wrongly consider only their excise revenue contribution, instead of their overall tax contribution which should include VAT and corporate taxes.) Introducing a traceability solution provides an opportunity to digitise more of the excise value chain, including, for example:

Building AI into the algorithms used.

The mandatory use of electronic invoicing.

Digital forensic investigation tools that enable users to view visual linkages, clusters and patterns; identify and extract key patterns in evidence like credit card numbers; perform content searches of data and metadata associated with a file, including ‘fuzzy’ searches; create dictionaries from seized data that can be used to guess passwords for password- protected documents; electronic discovery software to structure high volumes of unstructured data.

Automated electronic compliance checks or rules-based approaches to treat predefined risks (eg. automatically denying a claim, issuing a letter or matching a transaction).

Moving audit work to a virtual environment, including the electronic submission of audit-related documentation; and

The use of application programming interfaces.

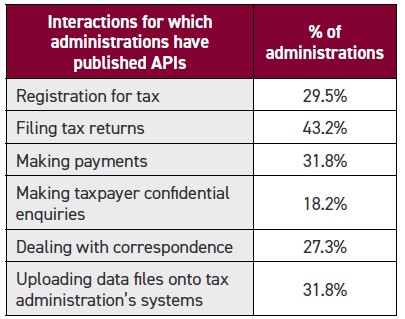

Application programming interfaces

The use of application programming interfaces (APIs) is gaining ground, with a significant 93% of administrations now deploying them to some degree (albeit not necessarily in respect of excise administration yet).

Protocols that allow for data to be shared between the administration and taxpayers/ traders automatically make interactions virtually seamless, in near-real time, ensuring connectivity and consistency throughout an entire ecosystem, and with built-in validation rules to improve data quality and reduce errors.

When APIs are used by an administration, they allow tax and customs obligations to happen as a by-product of a natural system like accounting software products, integrated with eg. point of sale systems.

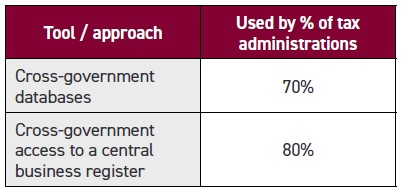

Data as an asset

The importance of managing data as a strategic asset is increasingly being recognised. To some extent, data is perhaps the single most important asset any tax and customs administration has; and their ability to collate, match and mine data their most important capability.

Of course, data is only truly useful to the extent that it enables an administration to make informed decisions about where best to focus its efforts, which requires the ability to collate information from a broad range of sources, including other government agencies; devices such as online cash registers; trip computers from trucks; gate registrations from weigh bridges; financial service providers; suppliers, using e-invoicing systems; and international partners.

At the same time, though, it is also important to be able to make sense of unstructured data like social media posts.

From a traceability solution perspective this poses both a challenge and an opportunity, simply because the typical supply chain of excisable goods tends to cut across all these different data sources. Implementing a secure marking and traceability solution has the potential to do more than just secure excisable goods – it has the potential to serve as a pilot project or proof of concept for the broader application of an integrated data management approach, that collates a broad range of disparate data sources in a way that allows for matching and mining, forming the basis of compliance risk management strategies and tactics.

Disruptive and emerging technologies

Tax and customs administrations tend to be late adopters of new technologies. However, in many quarters, administration is becoming increasingly professionalised and administrations are being run as agencies outside of the civil service, as a result of which more innovative practices are emerging. Some of the emerging technologies that are beginning to find traction include:

Blockchain, to secure traceability and end-to-end visibility, particularly from a risk analysis and targeting perspective.

Internet-of-things, for real-time monitoring of the movement of goods.

Artificial intelligence, to make sense of the ever-increasing volume of data, particularly for revenue collection models, audits, risk-based targeting, analysing x-ray images from container scanners, etc.

Virtual or augmented reality, to assist with the detection of fakes and counterfeits, or the visualisation of big data sets, and for training purposes.

Biometrics, for example to assist in verifying identities and access control, and identifying different actors in the supply chain, such as brokers, freight forwarders, and logistics operators.

Drones, for surveillance and monitoring purposes.

Leading edge traceability solutions will increasingly need to be aligned with and leverage emerging technologies.

Standing out in a crowd

The secure marking and traceability space is a relatively crowded one. The more successful providers are likely to be the ones that understand how their specific solutions contribute to a tax and customs administration’s broader mandates, beyond just securing the revenue stream from a few commodities. Doing this requires an understanding of what else is on their radar and speaking their language.

Telita Snyckers is an independent tax administration and illicit trade expert. Key clients include the International Monetary Fund, after having previously worked as an Executive at the South African Revenue Service, a compliance manager with the Inland Revenue Authority in Singapore and an associate with niche consulting firm Sovereign Border Solutions. She has a master’s degree in Constitutional Law and Fundamental Rights, is a certified Tax Administration Assessor, and has had work assignments in over 25 countries around the world. Her exposé on the role of big tobacco in fuelling illicit trade – Dirty Tobacco – was shortlisted for the prestigious Alan Paton / Sunday Times non-fiction award.

Subscriber content

Read the full article

Full access to Tax Stamp & Authentication News™ articles, newsletters and archives.