How Much Should Governments Be Paying for Track & Trace?

Although secure track and trace (T&T) systems are considered one of the most effective measures for reducing illicit trade, some governments are reluctant to implement them because of concerns about their cost.

A case in point relates to the WHO FCTC Protocol to Eliminate Illicit Trade in Tobacco Products, which requires all parties to establish secure T&T. While some governments are keen to join the Protocol, the costs of implementing T&T are holding them back.

What they are maybe failing to consider, however, is that T&T systems have often been shown to generate substantial returns on investment for governments that are already using them, which should provide reassurance to those governments still on the sidelines.

All well and good, but maybe what these governments also need is access to objective ROI analyses of T&T that are specific to their jurisdiction. Such analyses would then serve to support any subsequent plans to go ahead with T&T and could form the basis of an evaluation criterion in a T&T tender.

With this aim in mind, members of the Research Unit on the Economics of Excisable Products (REEP), based at the University of Cape Town, South Africa, have created a simulation model for determining what the cost per pack of a cigarette T&T system needs to be in order for governments to recover all costs associated with that system. The goal of the model, therefore, is to assist governments in the T&T procurement process by estimating the maximum cost of the system per pack (and hence per tax stamp – should they decide to use these).

As far as REEP is aware, no study has yet been conducted to compare the cost of T&T to the potential revenue generated from implementing a T&T system, which means that governments often rely on commercial reports and the experiences of other countries.

The simulation model developed by REEP has been applied to a study of the South African cigarette market, which currently has no tax stamp or T&T system in place and which is not party to the FCTC Protocol. However, this model can be adapted to other countries, as long as the appropriate data is available.

The premise of the model is that while T&T systems incur costs for implementation, they also generate additional revenue by diverting illicit cigarettes into the legal, taxed market. Therefore, there will be a T&T price at which the cost of T&T will be equal to the additional revenue generated by the newly taxed cigarettes. This is known as the breakeven cost.

Methodology

A three-stage, Excel-based methodology was used to develop the simulation model for South Africa.

The model assumes that the government will cover the entire cost of T&T, as opposed to passing it on to the tobacco industry, so as to simulate the highest possible cost that governments might face when implementing T&T, while still providing a breakeven point.

‘In addition, this assumption is fitting in many contexts, as involving the tobacco industry in implementing T&T could create opportunities for them to delay implementation or have a say in the T&T system selection, which could compromise the effectiveness of the operation,’ advised REEP, in a recent paper on the subject published in Tobacco Journal1.

Stage 1 – baseline

The first stage of the model, called the baseline, describes the cigarette market prior to T&T, in terms of size and segments of the legal market, approximate size of the illicit market, cigarette tax rates and structure, and average retail prices for legal and illegal cigarettes.

With regard to South Africa, the model includes four legal segments (imported, premium, popular and economy) plus an illicit segment. The baseline is an approximate average of the experiences of 2018, 2019 and 2021. 2020 was excluded because cigarette sales were banned for 20 weeks in that year, and the market was highly distorted.

The estimated size of the legal market in those three years was derived from the government’s national budget data. The market share and average price per segment were based on retail and Euromonitor data. While these estimates are subject to error, they are not crucial for the workings and outcomes of the model, advised REEP.

Academic studies indicate that illicit trade made up 30-35% of South Africa’s total cigarette market in this period. Although that percentage may have increased following the cigarette sales ban in 2020, the simulation assumes a 35% share of total market. It also estimates the average price of an illicit pack to be 19.60 South African rands (R) – or $1.24 – which is 70% of the average price of the cheapest legal pack.

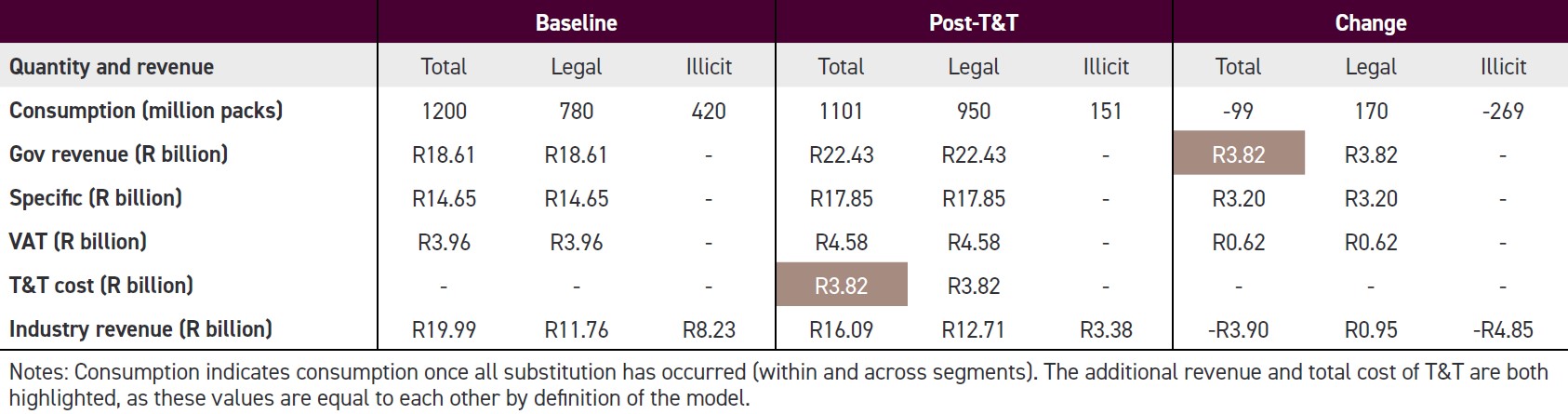

The revenues collected by the government and tobacco industry (defined as including both legal and illegal traders) are determined by multiplying each price element by consumption in the relevant market segment (see Baseline column in Table 1).

Stage 2 – price and consumption changes

The second stage of the model simulates changes in price and consumption as a result of deploying T&T. The key assumption is that T&T causes some portion of baseline illegal sales to move into the legal market.

For simplicity, the model assumes that the tax level and structure remain unchanged, so that all simulated changes are fully attributed to T&T.

The key parameters that determine changes in the market are:

1. The effectiveness of the T&T system (the proportion of illegal cigarettes captured by T&T).

2. The extent to which the tobacco industry changes retail prices (legal and illegal).

3. Price and cross-price elasticities of demand for legal and illegal cigarettes.

Regarding Parameter 1, the model assumes T&T is 60% effective, which is considered a conservative assumption in the case of South Africa, where most illicit products are manufactured within the country itself by legal entities.

For Parameter 2, the model assumes that the illicit price increases post-T&T, from 70% of the economy price to 80%. This is because, at its core, T&T is intended to make it more difficult for illicit trading to go unchecked; producers and vendors who continue to sell illegal cigarettes in the presence of T&T will face greater hurdles to continue these operations, and a greater risk of prosecution. As a result, traders will seek compensation for this increased risk, hence the increase in the price of illegal products.

Even though T&T does not directly impact the legal market, the price of legal cigarettes may also change in response to T&T as a strategic response by legitimate producers.

Various studies have shown that producers of legal cigarettes are often involved in illicit trade, and that illicit products provide important revenue streams for these companies, advised REEP. Since T&T is expected to cause a major reduction in the size of the illicit market, producers may change the price of legal products as they attempt to recover revenue lost from illicit products.

For the South African study, however, the model assumes the price of legal cigarettes remains unchanged.

Parameter 3 describes how consumers respond to a change in price. The price elasticity of demand for cigarettes quantifies how sensitive consumers in a particular segment are to a change in the price of that segment.

Stage 3 – new revenue levels

This stage of the simulation model involves the calculation of new levels of consumption and government revenues post-T&T.

At this point, the model uses Excel’s pre-programmed ‘Goal Seek’ function to calculate a T&T marker (eg. tax stamp) price such that total additional government revenue equals the total cost of T&T. This is the breakeven price of a marker.

In the case of South Africa, Table 1 shows that a T&T marker cost of R4.02 ($0.26) per pack results in additional government revenue of R3.82 billion ($242 million), which is exactly equal to the total cost of T&T. Therefore, the government breaks even.

Different scenarios

Some input assumptions, such as T&T effectiveness, are not well known. Because of this, the researchers ran nine scenarios based on six different assumptions, to provide a range of estimates for the T&T marker cost.

For T&T system effectiveness, it allowed for low (40%), moderate (60%) and high (80%) effectiveness. It also varied the legal tobacco industry’s response, allowing for a 10% decrease in the net-of-tax retail price, an unchanged price, and a 10% increase.

The results show that the effectiveness of the T&T system is the key variable in determining the cost per marker, and that the industry strategy has only a small impact on the marker cost.

From the nine scenarios, the breakeven marker cost is estimated between R2.68 ($0.17) and R5.24 ($0.34) per pack.

Securing an effective and industry- independent track and trace system for any price below this cost would generate additional revenue for government.

Implementing T&T is also assumed to result in a 5-11.5% reduction in overall consumption.

Comparison with actual T&T costs

The estimated minimum breakeven marker cost of R2.68 ($0.17) per pack is many times higher than the actual cost of existing T&T systems. For example, in Brazil the estimated cost is $0.016 per pack, while in Kenya it is $0.023 per pack. This means that a T&T system in South Africa is very likely to generate additional revenue, concluded the researchers.

To illustrate, they assumed that South Africa could secure a T&T system for R0.35 ($0.023) per pack, which is the price of the Kenyan system. If the system is 60% effective and the legal industry does not change prices, the government would collect an estimated R3.82 billion ($242 million) in additional revenue, while incurring a total cost of R333 million ($21 million); thus, net additional revenue would be R3.49 billion per annum. Even if T&T effectiveness is low and the industry increases prices, the government would make a net additional revenue of R2.04 billion ($130 million).

Even a T&T effectiveness as little as 4.5% would still generate net additional revenue for the government, assuming a marker cost of R0.35 (the cost in Kenya) and no change in retail prices, advised REEP.

Therefore, the government of South Africa should not be concerned about paying for a state-of-the-art T&T system, and the simulation should hopefully motivate it to join the FCTC Protocol.

While this paper presents a case for T&T implementation in South Africa, the model can produce similar simulations for other countries that are considering T&T. For those interested in having a model developed for their particular jurisdiction, please contact Kirsten van der Zee, REEP, [email protected], +27 82 648 9398.

1 - https://tobaccocontrol.bmj.com/content/tobaccocontrol/early/2022/09/14/tc-2022-057550.full.pdf, Kirsten van der Zee, Corné van Walbeek, Hana Ross.

Subscriber content

Read the full article

Full access to Tax Stamp & Authentication News™ articles, newsletters and archives.