The Pakistan Tax Stamp and Track & Trace System – Success or Failure?

Every government needs revenue to run the affairs of its country in the best possible manner. Tax evasion and leakages work like a parasite feeding off the overall wellbeing of citizens, which is why every government seeks to plug those leakages, and thus recover lost revenues.

Nowadays, Pakistan is grappling with profound problems affecting the very survival of the 220 million inhabitants of this Muslim country. These problems include a huge national debt, dwindling foreign exchange reserves, a large trade deficit, and high inflation coupled with political and economic instability.

The present government has one year left to deploy drastic economic measures for bringing about stability. One such measure involves a massive increase in both direct and indirect taxes, which will help the Federal Board of Revenue (FBR) reach its daunting 2022-23 revenue target of over PKR 7.47 trillion ($32.7 billion).

The FBR has implemented various initiatives for broadening the tax net, one of which is the imposition of a 10% super tax on large manufacturing units in the sectors of cement, sugar, steel, oil and gas, fertiliser, liquefied natural gas terminals, banking, automobiles, cigarettes, beverages, chemicals, as well as the airline sector.

One major initiative that has been dragging on, however, is Pakistan’s tax stamp and track and trace system.

A 17-year saga

The products initially identified for tax stamp systems were cigarettes, sugar, fertiliser, beverages, cement, and petroleum products, with a subsequent extension to iron and steel, and medicines.

Since 2005, FBR had been considering various proposals for addressing the evasion of federal excise duty and sales tax in the cigarette sector, and the best option identified was a system of affixing security stamps on each cigarette packet.

From 2005-2010, various trials were carried out in this regard, culminating in the launch of a track and trace project in 2013. However, this project remained unsuccessful due to a number of factors.

In particular, FBR officers lacked the knowledge required to draft documents such as requests for proposals and letters of intent, resulting in the FBR having to hire a consultant for drafting these documents, which took up a lot of time. This issue, coupled with a high level of industry resistance and lack of planning on the part of the FBR, is what led the country’s tax stamp and track and trace initiative to drag on for 17 long years – and several failed attempts at implementation.

It would therefore only be in 2021 that the FBR finally implemented a tax stamp and track and trace system (TTS), based on a March contract signed with a consortium between AJCL, Mitas, and Authentix, covering tobacco products, sugar, fertiliser, and cement.

TTS was launched in October 2021 on the tobacco products of Pakistan Tobacco Company (part of British American Tobacco) and was later extended to Phillip Morris and Khyber Tobacco Company.

As for sugar, TTS was installed in November 2021, with all sugar mills being supplied with tax stamps and application equipment. Then it was the turn of the fertiliser sector, in June 2022, with the cement sector scheduled to follow in October.

An estimated PKR 100 billion ($437.8 million) worth of evaded taxes was identified across the four sectors.

Components, processes, costs

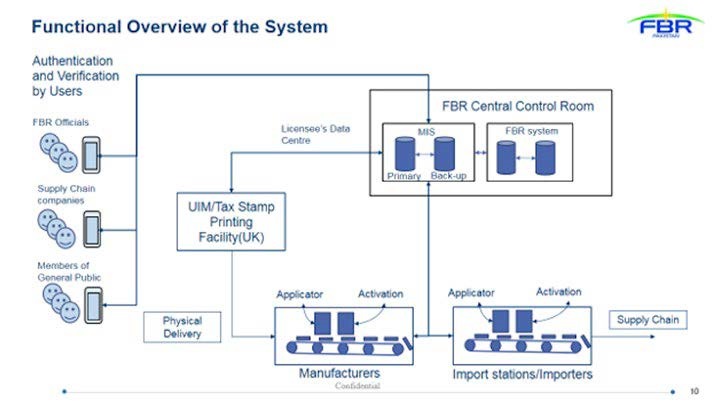

The system consists of the electronic monitoring of products in the four sectors, from their entry into the supply chain (ie. at the point of production or import), until their point of exit (ie. purchase by the end user).

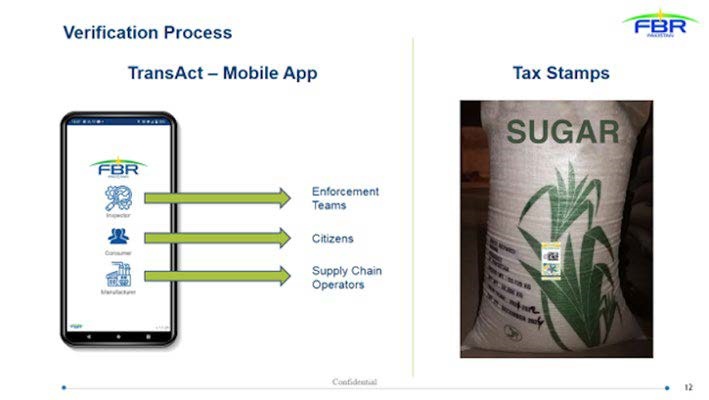

It entails the application of unique identification marks (UIMs) to the products, in the form of a 2D barcode and human- readable alphanumeric code, printed onto a tax stamp with covert, semi-covert, overt, and forensic security features.

The stamps and UIMs are securely produced in the UK and physically delivered to manufacturers and importers.

This means that no UIMs are ever sent as digital files for manufacturers to print onto the products themselves, thereby adding another layer of security to the UIM generation and application process.

The tax stamps/UIMs are applied to the product and activated during production, using equipment installed on each production line. The stamps must also be provided to foreign production lines for affixing to products imported into Pakistan. In cases where this is not possible, however, the affixing/activating process takes place at import stations within designated customs facilities.

The price of each tax stamp is PKR 0.76 ($0.0033), a cost which is borne by the manufacturer/importer.

A central database and management information system (MIS) has been established at FBR headquarters in Islamabad. The FBR has also set up (and is responsible for maintaining) communication links between the MIS and the UK printing facility, as well as links with manufacturing and import operations, and stakeholders out in the field.

A backup site has also been set up by the FBR in another building in Islamabad, where disaster recovery equipment (backup server and disks) has been installed under licence. The backup facility is connected to FBR HQ via a fibre optic link, or equivalent communication link with enough bandwidth to allow the immediate replication of the database.

The TTS accommodates the differences between production line dynamics and packaging types across the four industry sectors, including differences related to automation levels, production speeds, and the factory environment (level of control over dust, temperature, humidity, and vibration).

It also makes provisions for scaling in each sector to accommodate growth in product volumes and the size of organisations, and even to accommodate other areas of a particular industry, together with associated product types.

Enforcement

A crucial element of the TTS (and the difference between its ultimate success or failure) is the FBR’s Inland Revenue Enforcement (IREN) unit. The unit is responsible for a wide range of dedicated TTS enforcement activities including:

Monitoring stamping machines installed on production lines to ensure proper and uninterrupted TTS operation.

Examining and authenticating tax stamps.

Verifying reports of unauthorised production stoppage.

Securing non-operative production lines by means of a security seal.

Surveilling the production and movement of goods to ensure tax stamps are properly affixed and genuine.

Patrolling routes taken by goods along the supply chain to deter illicit trade.

Inspecting premises where specified goods are processed, stored, sold, or manufactured, including inspection of machinery, stocks, and accounts.

Stopping and searching vehicles used for carrying specified goods and seizing non- compliant goods.

Calculating duties and taxes applied to seized goods and initiating proceedings for their recovery.

An amount of PKR 4.35 million was allocated for the purchase of state-of- the-art equipment and latest technology gadgets for IREN squads to be able to do their job effectively.

Results

TTS is proving to be a comprehensive and robust electronic monitoring system, and a paradigm shift from conventional physical monitoring. The UIMs applied on industrial products have been found to help identify, isolate, and curb the production, supply, and movement of untaxed, counterfeit, and smuggled goods, thereby strengthening governance and rule of law.

In terms of numbers, the positive performance of TTS during 2021-22 compared to 2020-21 was demonstrated by an 11% increase in tax revenues.

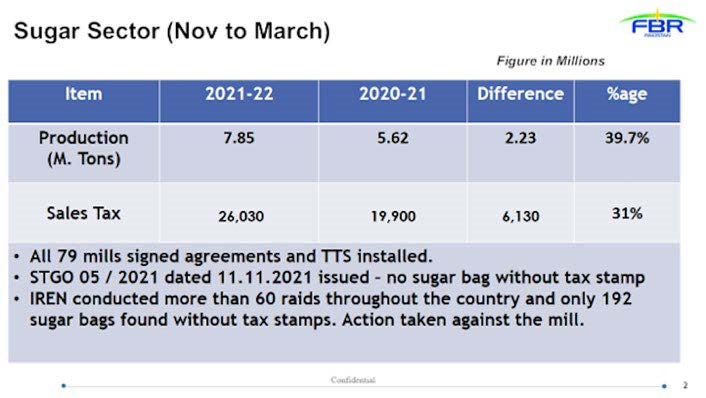

TTS in the sugar sector, in particular, has proved successful, as illustrated by the data in Figs 2 and 3.

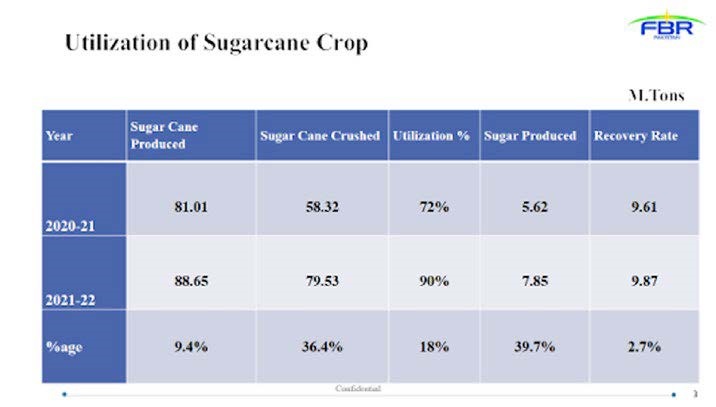

It is pertinent to highlight that the production data reported by the TTS is historically high. This was achieved as a result of high crop utilisation, which increased from 72% to 91%. This shows that it was very difficult for the sugar sector to suppress its production as no sugar bag was allowed to be removed from the factory premises without a tax stamp.

It goes without saying that the efforts of FBR officials and IREN squads made it difficult for tax evaders to underreport their production/sales, resulting in a tremendous growth in production data and collection figures from this sector.

Sales tax collection under TTS during the latest crushing season (December 2021-March 2022) amounted to PKR 26.03 billion ($114 million), as compared to PKR 19.9 billion for the previous season, representing a remarkable increase of 31%.

Similarly, sugar production was recorded at 7.85 million tonnes, compared to 5.62 million tonnes for the previous season, representing a 39.7% increase.

Not so smooth in tobacco sector

One could say that, as usual, things are not going as smoothly in the tobacco sector. Although three tobacco companies have implemented TTS, there are another 18 companies that are yet to sign a TTS agreement with the FBR, and that, as a consequence, have had their sales stopped.

Now that the FBR has mandated that all cigarettes must carry tax stamps from 1 July 2022, some tobacco companies have filed a case against the FBR, arguing that their stocks manufactured up to 30 June should be allowed to be sold without stamps.

The implementation of TTS in this sector had already been delayed after 12 cigarette manufacturers filed a previous case, demanding that the cost of implementing the system be borne by the FBR.

According to critics, the companies challenging the FBR are themselves engaged in illicit trade and fear that TTS will expose their illegal activities.

Conclusion

We can conclude that Pakistan has achieved partial success with regard to the tax stamp and track and trace system, largely thanks to its implementation in the sugar sector. Furthermore, now that TTS has been mandated on all cigarettes, the government is expecting to see a significant increase in tax collections in this sector as early as the first quarter (July- September 2022).

Going forward, stakeholders at government and manufacturer level (and particularly the present government), should focus on the benefits that can be achieved from successfully implemented systems – such as the one in the sugar sector – and look to extending TTS to other sectors during 2022-23.

For its part, the FBR is addressing all the bottlenecks and hurdles faced in the past, so as to ensure much smoother and faster implementation in these new sectors.

Such measures are urgently needed, given the precarious condition of Pakistan’s economy. In fact, what is actually needed is a quantum jump in revenue collection, in order to sustain the country post- COVID, as well as in light of the current economic impact of various national and international factors.

Subscriber content

Read the full article

Full access to Tax Stamp & Authentication News™ articles, newsletters and archives.